Health & Fitness

Newton Pensions: A Bigger Problem Than OPEB?

Newton Taxpayers Association's analysis and evaluation of how Newton has a structural spending problem regarding pension benefits.

From Joshua Norman

The City of Newton recently released its Contributory Retirement System Pension Plan Actuarial Valuation Analysis study for calendar year 2012. The trust’s fiscal year period is on a calendar year basis ending in December while the City of Newton’s fiscal year ends in June to coincide with the end of the school year. Public pension woes have been in the news lately.

- The Pioneer Institute recently created a new app evaluating Massachusetts’s state and municipal pension plans

- Detroit declared bankruptcy due to $20 billion in outstanding liabilities which included underfunded OPEB and pension plans

- CNBC reported about how public pension problems are a potential fiscal pandemic for taxpayers.

- Moody’s downgraded Chicago due to its $36 billion in outstanding pension liabilities ($18 billion net unfunded liability)

- The Competitive Enterprise Institute concluded that state and local governments collectively owe between $2.5 trillion to $4 trillion in net unfunded pension liabilities ($12,900 per capita nationwide)

We at the Newton Taxpayers Association remembered the buzz generated by Robert Mashal’s April article about Newton’s $601 million OPEB liability (“Next fiscal challenge for Newton is retiree benefits”) and we were aware of the Boston Herald’s recent editorial on municipal pension systems. This prompted us to evaluate Newton’s pension situation as we believe that Newton’s under-funded pension plan may be as big a problem or bigger than its unfunded OPEB plan.

Find out what's happening in Newtonwith free, real-time updates from Patch.

Municipal employees in Massachusetts aren’t eligible for Social Security based on their employment with a local government or school district. Municipal employees, teachers and school administrators that regularly work 20+ hours per week are required to contribute 5-11% portion of their earnings to fund their own retirements through a pension plan depending on hire date and salary earned. Teachers and school administrators outside of the City of Boston contribute to the Massachusetts Teachers Retirement System while Newton’s municipal department employees, school department aides, clerical employees and custodians contribute to Newton’s Contributory Retirement System.

We see good news, bad news, worse news and ugly news regarding Newton’s pension plan cash flow statement. The good news for Newton’s pension plan is its employee funded pension contributions into the pension trust fund grew by 70% cumulatively from 2000 ($4.6 million) to 2012 ($7.8 million). The bad news is that the City of Newton’s contributions of behalf of its employees increased by 125% cumulatively from 2000 ($7.3 million) to 2012 ($16.5 million). The worse news is that pension benefit and contribution refund payments made by the pension trust doubled from 2000 ($17 million) to 2012 ($34 million).

Find out what's happening in Newtonwith free, real-time updates from Patch.

We see good news, bad news, worse news and ugly news regarding Newton’s pension plan balance sheet. The good news is that Newton’s adjusted pension plan assets increased from $176.3 million in 1998 to $268.1 million in 2012 even with two major headwinds:

1) The stock market suffered two devastating crashes from 2000-2002 and 2007-2009.

2) Newton’s pension benefit payments exceeded contribution inflows by $100 million from 1998 to 2012.

The bad news is that Newton’s accrued benefit obligation more than doubled from 1998 ($240 million) to 2012 ($512.4 million). The worse news is that Newton’s projected pension benefit obligation (which includes accrued benefits earned and all benefits expected to be earned in future years by Newton’s active plan participants) is $595.2 million. The ugly news is that Newton’s net under-funded pension liability nearly quadrupled from 1998 ($63.7 million) to 2012 ($244.3 million) and its funded ratio dropped over 20% from 1998 (73.5%) to 2012 (52.3%).

Newton’s net under-funded pension liability is equivalent to $2,843 per Newton resident and $8,025 per taxpaying household. Although Newton is not alone in having an under-funded pension plan, we were shocked that Newton’s pension plan was in a weaker position than Hingham’s. However, after further review, we found that Hingham has been more proactive in reforming the management of its post-retirement benefit obligations than Newton. For example it outsourced the management of its pension plan assets to the state’s pension management board in 1986 versus 2007 for Newton. Hingham also began addressing its OPEB plan in 2009 versus 2011 for Newton.

Hingham’s plan is more financially sound than Newton’s based on these comparable metrics:

1) Funding Ratio: Hingham’s Funding Ratio of 69.4% is higher than Newton’s 52.3%

2) City Funded Contributions: Newton spent $542 per household while Hingham was able to spend $447 per household

3) Net Pension liability : Hingham’s net pension liability per household of $4,140 is nearly half of Newton’s $8,025 per household

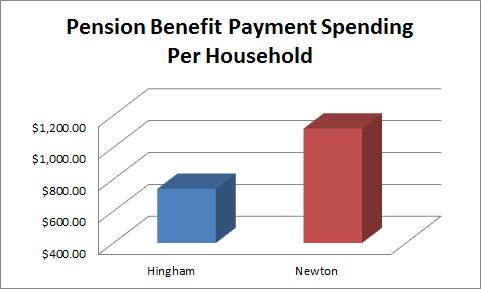

4) Pension Benefit Payments: Newton’s pension benefit payment spending grew by 62% since 2003 versus 42% for Hingham. Newton’s pension benefit payment spending per household was $1,117 versus $740 for Hingham.

5) Pension Trust Assets: Hingham’s pension trust fund has $9,415 in assets per household while Newton’s pension trust only has $8,806 per household

The Newton Taxpayers Association concludes that Newton has a structural spending problem with regards to its pension plan. Newton either needs to throttle back on its compensation growth in order to change the trajectory of its pension plan liabilities or take the lead in lobbying the legislature to allow municipalities to enact major reforms to its pension plan programs. We believe that Newton and other municipalities should be allowed to replace its defined benefit pension plans with cash-balance pension plans or defined contribution 403(b)/457 plans with an employer funded matching contribution, just like the private sector. We will follow up with a report on OPEB as we believe Newton’s pension trajectory is worse than its OPEB trajectory.